Interaction of supply and demand, equilibrium price and quantity

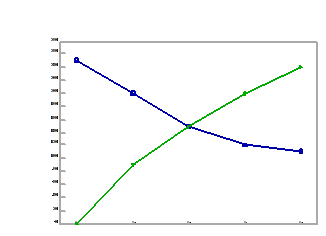

In perfectly competitive markets the market price is determined by the interaction of the forces of demand and supply. In such markets the price adjusts upwards or downwards to achieve a balance, or equilibrium, between the goods coming in for sale and those being requested by purchases. Demand and supply react on one another until a position of stable equilibrium is reached where the quantities of goods demanded equal the quantities of goods supplied. The price at which goods are changing hands varies with supply and demand. If the supply exceeds demand at the start of the week, prices will fall. This may discourage some of the suppliers, who will withdraw from the market, and at the same time it will encourage consumers, who will increase their demands. This is known as buyers market.

Conversely if we examine line D, where the price is £2 per kg, suppliers are only willing to supply 90kg per week but consumers are trying to buy 200 kg per week. There are therefore many disappointed customers, and producers realise that they can raise prices. This is known as sellers market. There is thus an upward pressure on price and it will rise. This may encourage some suppliers, who will enter the market, and at the same time it will discourage consumers, who will decrease their demand.

This can be shown by comparing the demand and supply schedule below.

|

|

Price of Commodity of X (£/kg)

|

Quantity Demanded of X (kg/week)

|

Quantity Supplied of X (kg/week)

|

Pressure on Price

|

|

A

|

10

|

100

|

20

|

Upward

|

|

B

|

20

|

85

|

36

|

Upward

|

|

C

|

30

|

70

|

53

|

Upward

|

|

D

|

40

|

55

|

70

|

Downward

|

|

E

|

50

|

40

|

87

|

Downward

|

|

F

|

60

|

25

|

103

|

Downward

|

|

G

|

70

|

10

|

120

|

Downward

|

A Twin force is therefore always at work to achieve only one price where there is neither upward or downward pressure on price. This is termed the equilibrium or market price:

The equilibrium price is the market condition which once achieved tends to persist or at which the wishes of buyers and sellers coincide.

Any other price anywhere is called DISEQUILIBRIUM PRICE. As the price falls the quantity demanded increases, but the quantity offered by suppliers is reduced, since the least efficient suppliers cannot offer the goods at the lower prices. This illustrates the third "law" of demand and supply that "Price adjusts to that level which equates demand and supply".