Reference no: EM1371878

Part-1

Suppose that the firm uses three inputs to produce its output: capital K, labor L and materials M. The firm's production function is given by

and the prices of capital, labor and materials are r=1, w=1 and m=1, respectively.

and the prices of capital, labor and materials are r=1, w=1 and m=1, respectively.

1. What is the solution to the firm's long-run cost-minimization problem given that the firm wants to produce Q units of output?

2. What is the solution to the firm's short-run cost-minimization problem when the firms wants to produce Q units of output and capital is fixed at K*?

3. When Q=4, the long run cost-minimizing quantity of capital is 4. If capital is fixed at K*=4 in the short run, what is the short-run cost-minimizing quantities of labor and capital?

Part-2

Peter gets $3 per week to spend as he pleases. Because he likes only peanut butter, p, and jelly, j, he spends the $3 on p (at a price of $0.05 per ounce) and j (at a price of $0.10 per ounce) in order to produce peanut butter and jelly sandwiches (PB&J). Bread is provided free of charge at home. Peter only eats PB&J sandwiches using 1 ounce of j and 2 ounces of p.

4. How much p and j will Peter buy with his $3 allowance?

5. Suppose that the price of j goes up to $0.15 per ounce. How much p and j will he now buy?

6. By how much should the allowance be increased in order for Peter to be compensated for the price increase in j described in part (5).

7. Graph your results of the previous three parts, using a figure with p in the vertical axis and j in the horizontal axis.

8. Discuss the results of this problem in terms of income and substitution effects in the demand for j.

Part-3

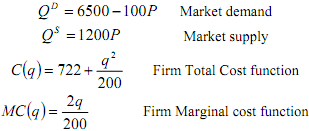

The long-run average cost for production of hard-disk drives is given by  where Q is the annual output of a firm, w is the wage rate for skilled assembly labor, and r is the price of capital services. The corresponding long-run marginal cost curve is

where Q is the annual output of a firm, w is the wage rate for skilled assembly labor, and r is the price of capital services. The corresponding long-run marginal cost curve is

. The demand for labor for an individual firm is

. The demand for labor for an individual firm is

The price of capital services is r=1.

9. In a long-run competitive equilibrium, how much output will each firm produce?

10. In a long-run competitive equilibrium, what will be the market price? Note that your answer will be expressed in terms of w.

11. In a long-run competitive equilibrium, how much skilled labor will each firm demand? Again, your answer will be in terms of w.

12. Suppose that the market demand curve is given by D(P) = 10,000/P. What is the market equilibrium quantity? Again, your answer will be in terms of w.

13. What is the long-run equilibrium number of firms? Again, your answer will be in terms of w.

14. Using your answers to parts (10) and (12), determine the overall demand for skilled labor in this industry. Again, your answer will be in terms of w.

15. Suppose that the supply curve for skilled labor used in this industry is *Γ(w) = 50w. At what value of w does the supply of skilled labor equal the demand for skilled labor you found in part (13)?

16. Using your answer from part (14), go back to part (9) to determine the long-run equilibrium price in this industry.

17. Using your answer from part (14), go back to part (11) to determine the long-run equilibrium quantity in this industry.

18. Using your answer from part (14), go back to part (12) to determine the long-run equilibrium number of firms in this industry.

Part-4

Assume that a firm is the unique producer in a market. This monopolist faces a demand curve P=210 - 4Q and initially faces a constant marginal cost MC 10.

19. Calculate the profit-maximizing quantity for this monopolist.

20. What will be this monopolist's optimal price?

21. What is the monopolist's total revenue at that price?

22. Suppose that the monopolist's marginal cost increases toMC 20. What is the monopolist optimal quantity now?

23. What will be the monopolist's optimal price?

24. What is the monopolist's total revenue at the price you found in part (e)?

Part-5

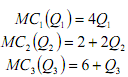

The inverse market demand function is P(Q) = 64 - Q/7. A multiplant monopolist operates three plants, with marginal cost functions:

25. Find the monopolist total marginal cost function MCT by horizontally adding up the marginal cost functions of the three plants.

26. Find the monopolist's profit-maximizing total quantity (i.e. the overall quantity he will produce taking into account its three plants).

27. Find the monopolist's optimal price.

28. Evaluate the monopolist total marginal cost function MCT at the above optimal (total) quantityQT .

29. Find the monopolist's profit-maximizing distribution of output among the three firms, Q1, Q2 and Q3.

Part-6

A competitive firm has the following short run total cost function:

Therefore, its associated marginal cost function is MC(q) = 3q2 -16q +30 �

30. Find the expression for the average total cost (AC) and the average variable cost (AVC).

31. Sketch MC, AC and AVC on a graph (a graph that approximates the pattern of these curves is enough).

32. At what range of prices will the firm supply zero output?

33. Identify the firm's supply curve on your graph.

34. At what price would the firm supply exactly 6 units of output?

Part-7

Suppose you are given the following information about a particular industry

Assume that all firms are identical, and that the market is characterized by pure competition.

35. Find the equilibrium price and the equilibrium quantity.

36. Find the output supplied by the firm, and the profit of the firm.

37. Would you expect to see entry into or exist from the industry in the long-run? Explain.

38. What effect will entry or exit have on market equilibrium?

39. What is the lowest price at which each firm would sell its output in the long run?

40. Is profit positive, negative, or zero if the firm sells its products for a price below the one you find? Explain

41. What is the lowest price at which each firm would sell its output in the short run?

Part-8 (Market structure and first-mover advantage) Assume for simplicity that a monopolist has no costs of production (MC=0) and faces a demand curve given by Q = 150 - P.

42. Calculate the profit-maximizing price-quantity combination for this monopolist. Also calculate the monopolist's profit.

43. Suppose instead that there are two firms in the market facing the demand and cost conditions just described for their identical products. Firms choose quantities simultaneously as in the Cournot model. Compute the outputs in the Nash equilibrium. Also compute market output, price and firm profits.

44. Suppose the two firms choose prices simultaneously as in the Bertrand model. Compute the prices in the Bertrand equilibrium. Also compute firm output and profit as well as market output.

45. Graph the demand curve and indicate where the market price-quantity combination from parts (a)-(c) appear on the curve.

46. Stackelberg competition. Assume as in the previous sections that firms have no production costs (MC=0), facing demand Q = 150 - P, and choose quantities q1 and q2. Compute the equilibrium of the Stackelberg version of the game in which firm 1 chooses q1 first and then firm 2 chooses q2.

47. Now add an entry stage after firm 1 chooses q1. In this stage, firm 2 decides whether or not to enter. If it enters then it must sink cost K2, after which it is allowed to choose q2. Compute the threshold value of K2 above which firm 1 prefers to deter firm 2's entry.