Reference no: EM131020806

Assignment - Managerial Accounting.

The exam consists of three assignments, that have to be solved completely.

The solution should be provided as a Winword file. Tables and/or graphs can be integrated. MS Excel can be used to make calculation. However, all spreadsheets should be included in your Winword file as tables. Please explain your solutions and give short interpretations of your results.

Please be aware that in the Excel sheets with the raw materials a comma is shown by "," (e.g., 24,32 ?) and the thousand sign by "." (e.g., 2.300 ? is 2300 ?).

Assignment 1: Budgeting and Variance analysis

The SCHIMAN-SKI GmbH is specialized on the production of skis for ambitious sportsmen. The production is structured in several steps that are allocated to the cost centers „Milling", „Grinding" and „Coating". For the cost center "Coating" the following costs are planned for the month January (in EuR):

|

Cost category

|

Total costs

|

Variable costs

|

Fixed costs

|

|

Direct materials

|

120,000

|

120,000

|

---

|

|

Overhead materials

|

46,000

|

30,000

|

16,000

|

|

Energy

|

32,000

|

24,000

|

8,000

|

|

Direct labor

|

184,000

|

184,000

|

---

|

|

Overhead labor

|

38,000

|

8,000

|

30,000

|

|

Social security

|

42,000

|

30,000

|

12,000

|

|

Depreciation & amor- tization

|

134,000

|

16,000

|

118,000

|

|

Other overhead

|

74,000

|

49,000

|

25,000

|

All cost data is related to a planned volume of 3,000 production hours resp. 5,000 produced pairs of skis per month. At the end of January the total actual costs are 15 % above the originally planned total costs. The actual volume has been 3,300 production hours which allowed to produce 5,500 pairs of skis.

Explore the causes for the variance between actual and planned costs! Please be aware that the firm uses a flexible budgeting system based on full costing. The capacity of the produc¬tion is estimated to be 5,500 pairs of skis per month.

Assignments:

a) Please determine the following figures for the cost center "Coating":

- Planned costs

- Actual costs

- Planned costs for a pair of skis

- Absorbed costs for the actual production volume

- Standard costs for the actual production volume

- Capacity utilization

b) Please calculate the following variances for the month January for the cost center "coating":

- Spending/efficiency variance

- Volume variance

- Total variance

Remark: Please indicate a positive sign for the spending/efficiency variance and for the total variance if actual costs are higher than planned costs and a negative sign in the case of cost savings. Please indicate a positive sign for the volume variance if too less fixed costs are allocated and a negative sign vice versa.

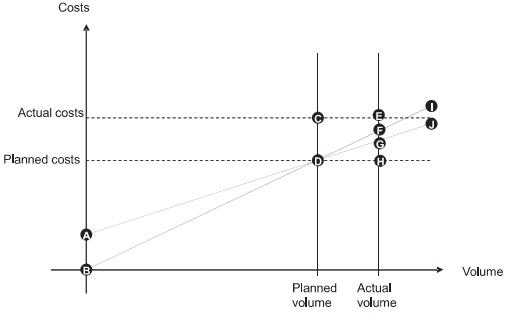

c) Please indicate using the following graph what points (e.g., C or D) indicate the standard costs and the absorbed costs at the actual production volume!

What lines (e.g., AD) stand for the spending/efficiency variance, the volume variance, the total variance, the fixed costs?

d) Please calculate the short-term and long-term lower price limit for a pair of skis for the planned volume!

e) For what production volume can we find the minimum variable and the minimum total costs for a pair of skis (unit costs)?

Assignment 2: Break Even Analysis

The fashion boutique BREUN & INGER sells menswear. The house is organized in two depart¬ments: the department Business Suits and the department Business Shirts. Mr. BREUN, the owner of the fashion boutique, is nervous because of bankruptcies of fellow entrepreneurs in stationary fashion retail. He also sees high growth in the online business, but modest or nega¬tive growth in stationary outlets.

The head of the department Business Shirts, HUGO Bosso, wants to know for his department how many shirts he has to sell per month to cover the costs of his department. His department makes monthly sales of € 495,000 with all shirts having an average price of € 90. The variable costs per shirt amount to € 30 on average. Furthermore, per month fixed costs of € 300,000 for the shirt department have to be covered (whereas € 50,000 EURO for the energy, € 100,000 for staff and € 150.000 for depreciation and amortization).

WOLFRAM JooD is head of the department Business Suits and is asked by Mr. BREUN to also assess the break even for his department. The department Business Suits sells four brands. In addition, fixed costs for the department of € 120.000 accrue per month. These fixed costs can¬not be allocated to the specific brands. The following data is available:

|

Suit brands

|

Price

per suit

(average)

|

Sales volume

per month

|

variable costs

per suit (average)

|

Fixed costs

for the brands

|

|

Lorenz Biagiotti

|

800 EUR

|

500 units

|

500 EUR

|

70,000 EUR

|

|

Jo Sander

|

700 EUR

|

100 units

|

600 EUR

|

9,000 EUR

|

|

Giovanni Rigatoni

|

2,000 EUR

|

40 units

|

800 EUR

|

10,000 EUR

|

|

Giorgio Armini

|

1,200 EUR

|

200 units

|

1,000 EUR

|

30,000 EUR

|

Assignments:

a) Please assess the break even volume for the department Business Shirts!

b) Please calculate the cash point for the department Business Shirts!

c) Regarding the actual situation, how much can the sales volume decline until the depart-ment is in the loss (safety margin)? How do you assess the situation of the department?

d) What is the target volume for intended net earnings of € 30.000 per month for the department?

e) Please calculate the lowest possible break even sales for the department Business Suits if you assume that the sales mix might change! For this, assume that all fixed costs can¬not be modified and are regarded as one entity!

f) Please calculate now the lowest possible break even sales for the department Business Suits for the case that now part of the fixed costs as indicated above can be allocated to the specific brands and can be modified when discussing the listing of the brand!

g) Please visualize your results from e) and f) in a graph! What can you derive from that for the risk exposure of the firm facing the trend to online sales?

h) What is the break even if the entire fashion boutique is considered as an entity? Make three suggestion to improve the situation of the firm.

Assignment 3: Activity Based Costing

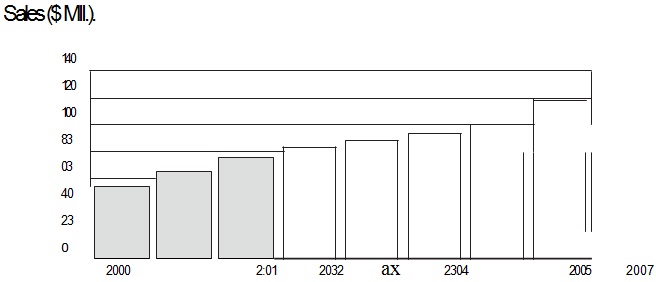

Micro Comp Inc. has been founded in 1998 by Steve Lobs in Boca Raton (Florida). In the first years of its existence the company did produce and sell standard micro computers. In the years following its market entry the company had a very substantial growth (figure 1).

Figure 1: Development of Sales of the Micro Comp Inc. (2000-2007)

The growing competition of Asian, especially Chinese and Japanese, suppliers forced the company in 2007 to specialize on customers specific computers for multi media and presentation purposes. An analysis of the micro computer market and a study of the production structure showed, that this market segment should have a higher profit margin.

However, the structure of the incoming orders changed dramatically since the company's foundation:

|

|

1998

|

2007

|

|

Special Microcomputer Standard Microcomputer

|

25

75

|

%

%

|

70

30

|

%

%

|

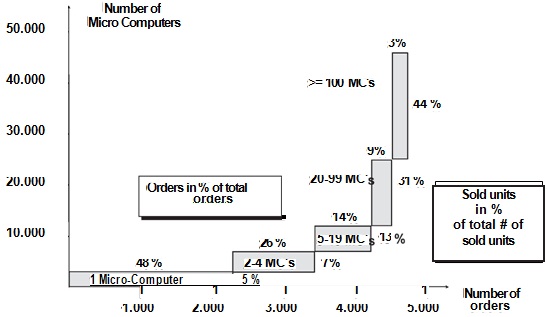

As the structure of the acquired orders was so different (Figure 2) the Company decided to substitute its traditional surcharge calculation by a activity based calculation. The manage¬ment expected a calculation that better fits with the cause principle and expected a better control of its activities.

Figure 2: Distribution of order size at Microcomp. Inc. in 2007

To make the implementation of the new cost accounting system efficiently the company fo¬cused on the cost categories overhead material costs, production related administration over¬head costs, sales overhead costs and service costs. These cost categories have been influenced by the change in strategy. The following figure 3 shows the change in the cost accounting system.

|

|

Surcharge

calculation

|

Change

|

Activity Based

Costing

|

|

Material

|

38,850

|

0

|

38,850

|

|

Overhead material costs

|

11,159

|

-11,159

|

|

|

Procurement

|

|

+5,665

|

5,665

|

|

Storage

|

|

+5,494

|

5,494

|

|

Direct production costs

|

13,650

|

0

|

13,650

|

|

Overhead production costs

|

13,056

|

0

|

13,056

|

|

Production relation

overhead administration costs

|

6,285

|

-6,285

|

|

|

PPS

|

|

+2,430

|

2,430

|

|

Quality audit

|

|

+3,855

|

3,855

|

|

Production costs

|

83,000

|

0

|

83,000

|

|

Sales costs

|

3,443

|

-3,443

|

|

|

Acquisition

|

|

+1,214

|

1,214

|

|

Calculation and offering

|

|

+690

|

690

|

|

Managing incoming orders

|

|

+339

|

339

|

|

Accounting

|

|

+302

|

302

|

|

Shipment

|

|

+898

|

898

|

|

Service costs

|

3,546

|

-3,546

|

|

|

Installation at customers

|

|

+2844

|

2,844

|

|

Maintenance

|

|

+702

|

702

|

|

General administration costs

|

15,011

|

0

|

15,011

|

|

Total unit costs

|

105,000

|

0

|

105,000

|

Figure 3: Change from the surcharge calculation to the activity-based calculation at MicroComp Inc. (all values in 1,000 $)

| Configuration driver process |

Cost driver |

Value of cost drivers (units) |

Process costs ($) |

Process costs per unit ($/unit) |

| Procurement |

Number of parts |

5,130,000 |

5,130,000 |

1 |

|

Number of interfaces |

53,550 |

535,500 |

10 |

| Storage |

Number of storage positions |

3,591,000 |

5,386,500 |

1.5 |

|

Number of interfaces |

53,550 |

107,100 |

2 |

|

(Total amount material overhead costs) |

-11,159,100 |

|

|

| PPS |

Number of construction plan |

1,215,000 |

|

|

| positions |

2,430,000 |

2 |

|

|

| Quality audit |

Number of standard modules |

450,000 |

3,150,000 |

7 |

|

Number of interface A |

26,800 |

294,800 |

11 |

|

Number of interface B |

17,800 |

249,200 |

14 |

|

Number of interface C |

8,950 |

161,100 |

18 |

|

(Total production related overhead administration costs) |

-6,285,100 |

|

|

| Installation at customer |

Number of special MC's |

31,500 |

2,331,000 |

74 |

|

Number of standard MC's |

13,500 |

513,000 |

38,00 |

| Maintenance |

Number of special MC's |

31,500 |

567,000 |

18 |

|

Number of standard MC's |

13,500 |

135,000 |

10 |

|

(Total service costs) |

-3,546,000 |

|

|

| Order driver process |

(Orders) |

($) |

($/Order) |

|

| Order acquisition |

Number of customer specific orders |

3,360 |

940,800 |

280 |

|

Number of standard orders |

1,440 |

273,600 |

190 |

| Calculation and offering |

Number of customer specific orders |

3,360 |

554,400 |

165 |

|

Number of standard orders |

1,440 |

135,360 |

94 |

| Managing incoming orders |

Number of customer specific orders |

3,360 |

255,360 |

76 |

|

Number of standard orders |

1,440 |

83,520 |

58 |

| Accounting |

Number of orders |

4,800 |

302,400 |

63 |

| Shipment |

Number of orders |

4,800 |

897,600 |

187 |

|

(Total sales costs) |

-3,443,040 |

|

|

|

(Total process costs) |

-24,433,240 |

|

|

|

|

|

|

|

| Structure of process utilization per unit |

Special-MC (31,500 units) |

Standard-MC (13,500 units) |

|

Parts |

120 |

100 |

|

|

Interfaces (A, B, C) |

A, B and C |

None |

|

|

Storage positons |

84 |

70 |

|

|

Constructing plan positions |

30 |

20 |

|

|

Standard modules |

10 |

10 |

|

Figure 4: Evaluation of process unit costs

|

A) Traditional surcharge calculation

|

|

Costs (surcharge)

*

|

Special

|

Standard

|

|

Direct material costs*

|

951.00

|

744.00

|

|

Overhead material costs (28.72 %)

|

273.16

|

213.70

|

|

Direct production costs (DPC)*

|

305.00

|

275.00

|

|

Overhead production costs (OPC)(95.65 % on

|

291.73

|

263.03

|

|

DPC)

|

|

|

|

Production related overhead administration costs

|

140.43

|

126.62

|

|

(23.53 % on DPC and OPC)

|

|

|

|

Production costs (PC)

|

1,961.32

|

1,622.36

|

|

Sales costs (4.15 % on PC)

|

81.36

|

67.30

|

|

Service costs (4.27 % on PC)

|

83.79

|

69.31

|

|

General administration costs (18.09 % on PC)

|

354.72

|

293.41

|

|

Total costs of order

|

2,481.19

|

2,052.38

|

|

Total unit costs

|

2,481.19

|

2,052.38

|

Figure 5: Example for calculation of 1 standard Micro Computer and 1 customer specific Micro Computer with 3 interfaces A, B, C

* Installing the interfaces in the special MC additional to the standard MC following direct costs are produced:

|

Material |

Wages |

| Interface A |

38 |

8 |

| Interface B |

64 |

10 |

| Interface C |

105 |

12 |

| Total |

207 |

30 |

|

B1) Surcharge calculation with integrated ABC (order size 1 unit)

|

|

Costs (surcharge)

|

Special

|

Standard

|

|

Direct material costs

|

951.00

|

744.00

|

|

Overhead material costs

|

|

|

|

Procurement

|

150.00

|

100.00

|

|

Storage

|

132.00

|

105.00

|

|

Direct production costs

|

305.00

|

275.00

|

|

Overhead production costs (95.65 % on DPC)

|

291.73

|

263.03

|

|

Production related overhead administration costs

|

|

|

|

PPS

|

60.00

|

40.00

|

|

Quality audit

|

113.00

|

70.00

|

|

Production costs (PC)

|

2002.73

|

1597.03

|

|

Sales costs

|

|

|

|

Acquisition

|

280.00

|

190.00

|

|

Calculation and offering

|

165.00

|

94.00

|

|

Managing incoming offers

|

76.00

|

58.00

|

|

Accounting

|

63.00

|

63.00

|

|

Shipment

|

187.00

|

187.00

|

|

(Total)

|

(771)

|

(592.00)

|

|

Service costs

|

|

|

|

Installation at customers

|

74.00

|

38.00

|

|

Maintenance

|

18.00

|

10.00

|

|

(Total)

|

(92.00)

|

(48)

|

|

General administration costs (18.09 % on PC)

|

362.20

|

288.83

|

|

Total costs of orders

|

3,227.93

|

2,525.87

|

|

Total unit costs

|

3,227.93

|

2,525.87

|

Assignments:

The Micro Comp Inc. has got two calls for offers.

The first customer wants to know, what either 10 standard Micro Computers (no interfaces) or 10 Micro Computers with customer specific layout (with all three interfaces A, B, C) will cost.

Another customer is interested to have either 20 Micro Computers in the standard form (no interfaces) or 20 customer specific Micro Computers (with all three interfaces A, B, C).

a) Please calculate the unit costs for one standard Micro Computer or specialized Micro Computer for both customers (order size 10 and order size 20) using the activity based calculation!

b) Compare both orders for the effect of complexity and for the effect of degression and calculate both effects on your results of a)!

c) What conclusions can be drawn from your analysis? What are limitations for your conclusions? Please discuss and explain your results!

Attachment:- Raw data.xls