Individual firm and market supply curves

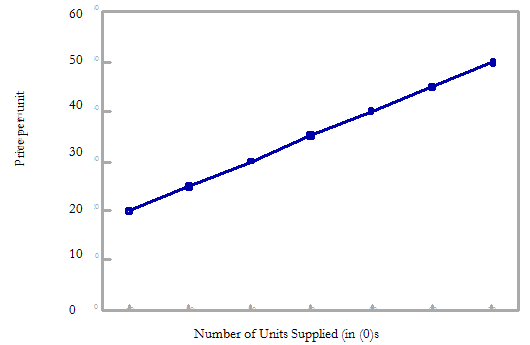

The quantities and prices in the supply schedule can be plotted on a graph. Such a graph is called the firm supply curve.

A firm supply curve is a graph relating the price and the quantities of a commodity a firm is prepared to supply at those prices.

The typical supply curve slopes upwards from left to right. This illustrates the second law of supply and demand "which states that the higher the price the greater the quantity that will be supplied".

More is supplied by the firms which could not make a profit at the lower price.

Fig : The firm supply curve

The market supply curve is obtained by horizontal summation of the individual firm supply curves i.e. taking the sum of the quantities supplied by the different firms at each price.

Consider, for the sake of exposition, an industry consisting of two firms. At price P1, firm I (diagram below) supplies quantity q1, firm II supplies quantity q2, and the total market supply is q1+q2

At price P2, firm I supplies q'1, firm II supplies quantity q'2, and the total market supply is q'1+q'2,. SS is the total market supply curve.