Evaluate the equilibrium price and quantity

(a) Find the equilibrium price and quantity

(b) If government in trying to control the price of the good fixes the price at c550

(i) Explain the type of price control the government has applied using an appropriate diagram.

(ii) Calculate and explain the type of excess which will result from the price control.

(iii) Give three (3) problems that the excess in (ii) may cause.

Answer

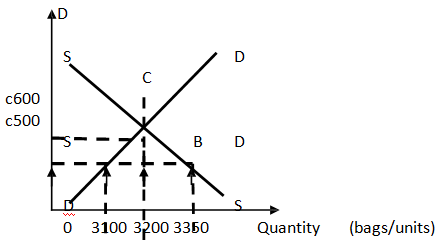

(a) Given the demand function QD= -3P + 5000 and the supply function as

Qs = 2P + 2000. At equilibrium , QD = QS

-3 + 5000 = 2P + 2000

5000 - 2000 = 2P + 3P

3000 = 5P

3000/5 = P P = c600

Therefore

Q = 2(600) + 2000

Q = 1200 + 2000

Q = 3200 bags/units

The equilibrium price and quantity are c600 and 3200 units respectively.

(N) or cedi (C) for price

(i) If government fixes the price of the good at c550, this will be a maximum price control. This is because c550 is below the equilibrium price of c600.

(ii) At the price of c550.

QD = -3P + 5000 = -3(550) + 5000 = -1650 + 5000 = 3350 bags/units

Qs = 2(550) + 2000 =1100 + 2000 = 3100 bags/units

Excess demand = QD – Qs = 3350 – 3100 =250 bags/units

At the maximum price of c550, quantity demanded of 3350 bags/units exceeds the quantity supplied of 3100 bags/units resulting in an excess demand of 250 bags/units .