Reference no: EM13671028

Part -1:

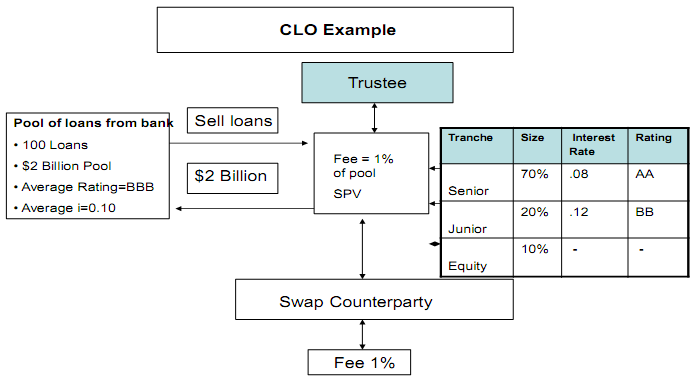

What is the expected Return on Equity for the equity tranche in each of the first two years of a five year CLO (Collateralized Loan Obligation)?

Information:

- $2.0 billion dollar pool.

- Fees are paid at the end of the year and are 1% (of face value) in the first year and 1% (of face value) in the second year.

- Assume that the defaults occur at the beginning of the second-half of each year.

- The recovery from the defaults is invested immediately at (5%).

- The annual interest on the pool of loans (i=10%) is paid semiannually and is based on the remaining balance of loans in the pool.

- The default rates and recovery rates are provided below: Losses are not reduced from equity until the end of the CLO.

Year One Year Two

Default Rate 3% 8%

Recovery Rate 40% 40%

Part -2:

1. Target forwards were discussed in the context of the Aracruz case. To recall, a target forward is a variant on the plain vanilla forward contract structure and represents a very aggressive bet on direction. For specificity, consider a short target forward position. If the delivery price in the contract is K and the price of the underlying at maturity is Sr, the payoff to a typical short target forward is

K - ST, if K > ST

2(K - Sr), if K< Sr

In these payoffs, the loss from a price increase (K < SO increases twice as fast as the gain from a price decrease (K> Sr), implying that the holder of this position is betting aggressively against a price increase.

In contrast, a vanilla forward contract has a linear payoff. The payoff to a short vanilla forward is just

K - ST

or, writing it more elaborately, the payoff is

K - ST, if K > ST

K - ST, if K < ST

Show that the target forward is the same thing as holding (a) a short position in a vanilla forward, and (b) a short position in a plain vanilla option. (Hint: Take the difference in payoffs between the payoff of a target forward and a vanilla forward and see what this looks like. Your answer must be precise on which vanilla option -a short call or a short put - should be combined with the short forward to create a short target forward.)

2. A principal-protected note is a note that guarantees its holder the return of the principal amount at maturity. The coupon on these notes is typically variable and is linked to the performance of a risky asset such as an equity index. Such notes are popular with investors because they allow for upside participation in risky assets while limiting downside risk. This question shows how a principal-protected note may be decomposed into a combination of a straight investment and an option, and therefore how it may be priced.

Consider a principal-protected equity-linked note. The note guarantees principal repayment at maturity together with a coupon that depends on the returns on a specified equity basket, say the S&P 500 index.

For specificity, consider the following structure. The initial price of the note is $100. At the end of a year, the note promises holders repayment of the principal amount of $100, and a coupon equal to a fraction a of the returns on the S&P 500 index over the year, provided these returns are positive. If the S&P 500 has negative returns over the year, the note pays no coupon. Thus, investors in the notes are able to participate partially in the upside of the index but are fully

protected against declines in the index.

To put this in notational terms, let So denote the level of the index at inception of the note, and for simplicity set So = 100. (This is just a normalization.) Let Sr denote the level of the index at maturity of the note. Then, the coupon on the note is

{ a x (ST -So), if ST > So

0, otherwise

[For example, if a = 0.75, the note promises the holder 75% of the returns on the S&P 500. So for instance, if the index goes up by 10% over the one-year life of the note (from So = 100 to ST = 110), investors in the notes will receive a 7.50% or $7.50 coupon. But if the index has zero or negative returns in that period (i.e., if Sr 5 100), investors receive a zero coupon payment.]

The objective of this exercise is to determine the "fair value" of a. Use the following steps.

1. Describe in a diagram the total payoff received by the holder of the note at maturity as a function of the level Sr of the index at that point.

2. Show that this payoff is the same as the payoff received from holding a portfolio of the following instruments: x axis , y equals to 100

a. A zero-coupon bond with a face value of $100 and a maturity of one year.

b. a units of a one-year at-the-money call option on the index, i.e., a units of a call option with a strike of 100 and a maturity of one year.

3. Thus, the initial price of the note must be the same as the sum of the prices of these two instruments. That is, denoting the initial price of the zero-coupon bond by P and the initial price of a one-year at-the-money call option by C, we must have

P+aC=100

4. Suppose the risk-free one-year interest rate is 5% expressed in simple terms. That is, $1 invested at the beginning of the year grows to $1.05 at the end of the year. What is the value of P? Present value equation

5. Suppose further that market price C of a one-year at-the-money call option on the index is C = 6.89. What then is the "fair value" of a, i.e., the value of a that satisfies equation (1)? Solve the problem by plugging the data

6. Finally, consider the position of the bank that has sold this principal-protected note to investors. how volatility affects options

a. Does the bank gain or lose if volatility in the stock market increases?

b. Assuming the bank can take long and/or short positions in call and put options on the index, how can the bank hedge its risk?

3. As in the Metallgesellschaft case, this question concerns cash flow risk arising from pricing strategies. Metallgesellschaft allowed its customers to lock in a fixed price for future delivery of refined oil, which left the company exposed to increases in the price of crude oil. The scenario below considers a situation where customers are given a choice of price.

A company manufactures and supplies gold wire to customers. Delivery is made one month after the customer order is received. Company practice is to buy gold on the day the order is received. Let date 0 denote the date of order and date T denote the date of delivery.

Customers are given a choice between date-of-order and date-of-delivery price. (The choice is made after the date of delivery price is known.) Specifically, if Go represents gold price on the date of order and Gr represents gold price on the date of delivery, customers can choose between paying Go + K and GT+ K, where K is a fixed margin.

For simplicity, suppose that the company has no other costs of production; the only cost is the cost Go of buying the gold when the order is received. Thus, if the customer chooses date-of order pricing, the company's profit on the order is

(Go + K)- Go= K,

while if the customer chooses date-of-delivery pricing, the company's profit on the order is

(GT + K)- Go = K - (Go - GT).

Answer the following questions:

1. Is there directional risk in offering customers this pricing choice? Of what sort? That is, does the company gain or lose if gold pricesgo up? If they go down? what kind of derivative this one lookslike

2. Is there volatility risk? That is, does the company gain or lose if gold prices become more volatile?

3. In the language of derivatives, what kind of option on gold has the company implicitly sold its customers? Put differently, assuming there are standard call and put options available on gold, what kind of option could the company use to hedge its cash flow risk?

What is the exact opposite to hedge?