INTERPRETING THE SIMPLEX TABLEAU

We can now see that our attention must be directed to reading, interpreting and analyzing the (simplex) results. It is erroneous, however, to assume that only one can interpret the simplex tableau without having adequate knowledge of how and why the simplex method works.

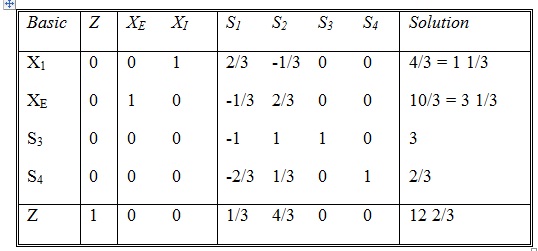

It will be disappointing to you to think that all we can get out of the optimum simplex tableau is a list of variables and their optimum values. The fact is that the simplex tableau is "loaded" with important information, the least of which are the optimum values of the variables. The following list summarizes the information that can be obtained from the simplex tableau, either directly or with simple additional computations.

1. The optimum answer

2. The position of resources

3. The unit value of each resource

4. The sensitivity of the optimum answer to changes in availability of resources, coefficients of the objective function, and usage of resources by activities.

The first three items are readily available in the optimum simplex tableau. The fourth item requires additional computations that are based on the information in the optimum solution.

To demonstrate these items we use the same example, which we repeat here for convenience.

The optimum tableau is specified as:

Maximise: Z = 3XE + 2X1

Subject to: XE + 2X1 + S1 = 6

2XE + 2X1 + S2 = 8

-XE + 2X1 + S3 = 1

X1 + S4 = 2

X1, XE, S1, S2, S3, S4 ≥ 0