Reference no: EM131193570

Instructions to candidates:

1. Print your name and student number on your work as well as the assignment cover sheet which is available from the Business School office;

2. Attempt any five (5) questions;

3. Submit by the due date as provided in the course description;

4. Please reference all copied diagrams, formula, definitions and quotations or direct extracts.

Question 1:

(a) Suppose that oil prices rise sharply for years as a result of a war in the Middle East. Illustrate with a diagram what happens to the:

(i) Demand for automobiles?

(ii) Demand for home insulation?

(iii) Demand for coal?

(iv) Demand for tyres?

(v) Demand for bicycles?

(b) Explain the impact of external costs and external benefits on resource allocation;

(c) Why are public goods not produced in sufficient quantities by private markets?

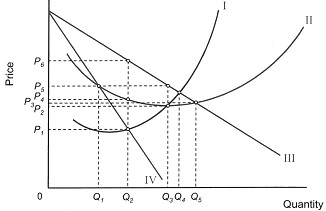

Question 2:

The following diagram illustrates a firm under monopolistic competition.

(a) Label the curves.

Curve I Curve II

Curve III Curve IV

(b) Does the diagram represent the short-run or long-run position? Short-run / Long-run

(c) Is P3 the long-run equilibrium price? (1 marks) (explain)

(d) What are the profit maximising output and price?

(e) On the diagram, shade in the amount of profit made at the maximum-profit output.

(f) Draw new average and marginal revenue curves on the diagram to illustrate the long-run equilibrium that will occur after the entry of new firms into the industry.

(g) What is the relationship between the AC, MC, AR and MR curves at this long-run equilibrium position? Explain.

Question 3:

(a) Explain why scarcity forces individuals and society to incur opportunity costs. Give specific examples.

(b) Suppose a chocolate bar manufacturer promotes its products by advertising and opportunity to win a 'free car'. Is this car free because the winner pays zero for it? Illustrate and explain using a diagram.

(c) Why is the production possibility frontier bowed outwards?

Question 4:

Suppose electricity prices increase significantly over a two year period as a result of the government introducing a carbon tax that raises the costs for coal-fired power stations. Illustrate and explain using diagrams, what happens to:

(a) Demand for domestic gas?

(b) Demand for solar powered cars?

(c) Demand for air conditioners?

(d) Demand for home insulation?

(e) Demand for outdoor swimming pools?

Question 5:

In some large cities, motorists pay a fee when they bring their vehicles into the busiest part of the city (congestion charge).

(a) Illustrate with a diagram and explain how this charge is an example of the price system at work;

(b) How do you think that the authorities would determine the level of the charge if they have a particular target for the reduction in the number of vehicles entering the congestion charge zone?

(c) Given that revenues from these congestion charges are invested in the city's transport system, how will this affect the charge level holding all other variables constant?

Question 6:

(a) Suppose the income elasticity of demand for pre-recorded music compact disks is +7 and the income elasticity of demand for a cabinet maker's work is +0.7. Compare the impact on pre-recorded music compact disks and the cabinet maker's work of a recession that reduces consumer incomes by 10 per cent.

(b) How might you determine whether MP3 music players and the pre-recorded music compact-discs are in competition with each other?

(c) Interpret the following Income Elasticities of Demand (YED) values for the following and state if the good is normal or inferior;

YED= +0.8 YED= -2.4

(d) Interpret the following Cross-Price Elasticities of Demand (XED) and explain the relationship between these goods.

XED= + 0.85 XED= -4.5

Question 7:

(a) Discuss the following statement: 'In the real world, there is no industry which conforms precisely to the economist's model of perfect competition. This means that the model is of little practical value'.

(b) Illustrate with a diagram and explain the short-run perfectly competitive equilibrium for both (i) individual firm and (ii) the industry.

(c) Illustrate with a diagram and explain the long-run perfectly competitive equilibrium for the firm.

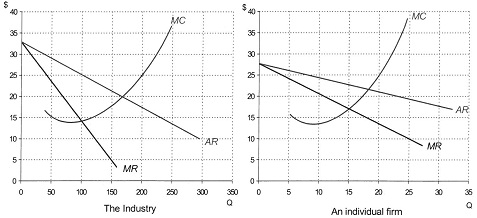

Question 8:

The following diagrams illustrate an industry under oligopoly consisting of 10 equal-sized firms and a particular firm in that industry. Each of the firms produces an identical product.

(a) Assuming that the firms form a cartel, what price will the cartel choose if it wishes to maximise overall profits for the cartel?

(b) What total output must the cartel produce in order to maintain this price?

(c) To what output will an individual firm be restricted if this price is to be maintained (assume all firms are permitted to produce the same level of output)?

(d) If the other firms stick to this output, how much would an individual firm be tempted to produce if it wished to maximise its own profit at the agreed price?

(e) If it undercut the cartel price, what price and output would maximise its profit (assuming that the other members did not retaliate?